News

Three upcoming changes in the photovoltaic industry

Release time: 2022-01-30

Source: Market value observation

From January to November 2021, the installed capacity of domestic PV increased by 34.8GW, with a year-on-year growth of 34.5%. Considering that nearly half of the installed capacity in 2020 was occurred in December, the annual growth rate in 2021 will be far lower than the market expectation. The China Photovoltaic Industry Association forecasts the annual installed capacity to be 45-55GW, down by 10GW, that is, the worst will fall by 6.6% year-on-year, and the best will increase by 14%.

2021 is the first year of the 14th Five-Year Plan. The industry previously estimated that the average annual installed capacity of PV in the "14th Five-Year Plan" was between 70-90 GW. After the goal of carbon peaking in 2030 and carbon neutralization in 2060 was proposed, it was widely believed that the photovoltaic industry would usher in a historic golden development cycle, but the price rise throughout 2021 caused an extreme industrial environment. The PV industry chain consists of five links from top to bottom, which are roughly divided into four manufacturing links: silicon material, silicon wafer, cell and module, and power station development. Starting from 2021, the high price of silicon materials will be transferred to silicon wafers and battery wafers in turn, and the price of auxiliary materials such as superimposed glass, EVA film, backplane and frame will rise. The price of components was pushed back to 2 yuan/W three years ago while 1.57 yuan/W in 2020. In the past decade or more, component prices have basically followed the logic of unilateral downward movement. The price reversal in 2021 has restrained the willingness of downstream power stations to install. In the future, the unbalanced development of all links of the PV industry chain will continue. Ensuring the safety of the supply chain is an important issue for all enterprises. Large price fluctuations will reduce the performance rate and damage the credibility of the industry.

Based on the downward expectation of the price of industrial chain and the huge project reserve in China, the PV Industry Association estimates that the new installed capacity of PV will probably exceed 75GW in 2022. Among them, the distributed photovoltaic is taking shape.

Stimulated by the dual-carbon target, capital scrambles to invest in photovoltaic, a new round of capacity expansion has begun, and structural surplus and imbalance still exist, and may even intensify. Competition between old and new players and restructuring of the industry pattern are inevitable.

At the manufacturing end, there is still a good year for the silicon material link, and the era of high profits in the silicon chip link is coming to an end. At the power station end, distributed power stations will become the leading role, and the development will also be standardized. At the enterprise end, it is the competition between LONGi and Tongwei, the two leading enterprises. It is unknown who will become the first. While other old players will face fierce competition with new players.

Silicon material still has a good year

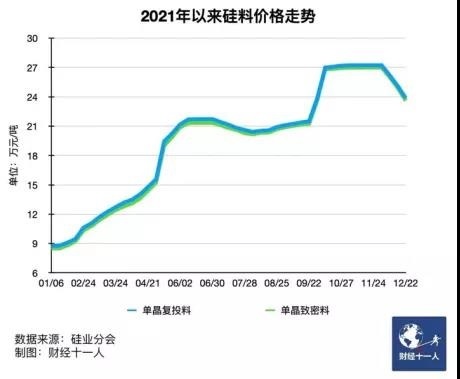

Under the price increasing in 2021, the four major links of photovoltaic manufacturing end were uneven. From January to September, the prices of silicon materials, silicon chips, battery chips and modules increased by 165%, 62.6%, 20% and 10.8% respectively. The price rise is due to the shortage of silicon materials. The highly concentrated silicon chip enterprises received dividends in the first half of the year. However, profits shrank in the second half of the year due to the release of new production capacity and the depletion of low-cost inventory. The cost transfer ability of battery and module side is obviously weaker, and the profit is seriously damaged.

With the opening of a new round of capacity competition, the profit distribution at the manufacturing end will change in 2022: silicon materials will continue to earn, silicon chips will compete fiercely, and the profits of batteries and components are expected to be repaired. Next year, the supply and demand of silicon materials will remain in a tight balance as a whole, and the price center will move downward, but the link will still retain a high profit. The total supply of silicon material of about 580,000 tons in 2021, which basically matches the demand for terminal installation. However, compared with the silicon chip end with a capacity of more than 300 GW, it is in short supply, which leads to the phenomenon of scrambling for materials, hoarding materials and boosting prices in the market. Although the high profit of silicon material in 2021 has led to the expansion of production, due to the high entry threshold and long expansion cycle, the gap between its capacity and the silicon chip end will still be obvious next year.

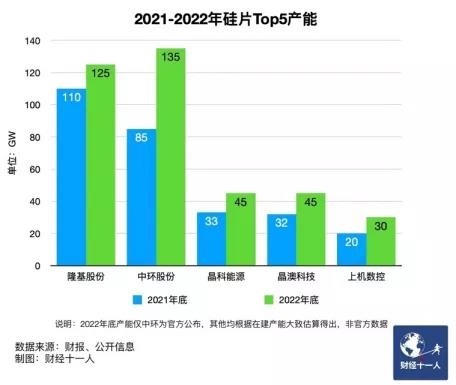

According to the preliminary statistics made by the Silicon Industry Branch according to the plans of major enterprises, the domestic polysilicon capacity will reach 850,000 tons/year by the end of 2022. Considering the overseas capacity supply, it can meet the installation demand of 230GW. According to incomplete statistics and calculations by Caijing reportor, the Top5 silicon chip enterprises alone will add about 100GW of capacity by the end of 2022, and the total silicon chip capacity will be nearly 500GW.

Zou Yanhui, a green energy industry analyst at TrendForce, pointed out that, considering the pace of capacity release, double control indicators of energy consumption, maintenance and other uncertain factors, the silicon material capacity in the first half of 2022 is limited, and the supply shortage will be effectively alleviated in the second half of 2022 due to the tight balance between supply and demand due to the downstream rigid demand. In terms of silicon material price, Great Wall Securities expects that the silicon material price will decline steadily in the first half of 2022, and will accelerate in the second half of 2022. The price center of the whole year may be 150,000 to 200,000 yuan/ton. Although this price has declined compared with 2021, it is still at an absolute high level in history, and the capacity utilization and profitability of leading manufacturers will also remain at high levels.

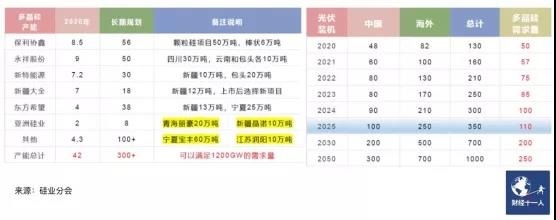

Stimulated by the price, almost all domestic silicon enterprises have put forward a large expansion plan. Generally speaking, the production cycle of the silicon material project is about 18 months, the capacity release speed is slow, the capacity elasticity is small, and the start-up and shutdown costs are high. Once the terminal starts to adjust, the silicon material link will fall into a passive position. The Silicon Industry Branch has warned against excessive investment. The short-term supply of silicon materials continues to be tight, the production capacity will continue to be released in the next 2-3 years and in the medium and long term, supply may exceed demand. At present, the planned capacity announced by the silicon material enterprise has exceeded 3 million tons, which can meet the installation demand of 1200GW. Considering the huge capacity under construction, the good market situation of silicon material enterprises is likely to be only 2022. The price fluctuation of the photovoltaic industry chain in 2021 has seriously affected the stable development of the industry. In this regard, the relevant leaders of the Ministry of Industry and Information Technology and the National Energy Administration have made statements recently, pointing out that stable supply and stable prices of the industry chain are not only the common expectation of the whole industry, but also in line with the common interests of the whole industry.

The era of high profits for silicon wafers is over

In 2022, the silicon chip link will suffer from the rapid expansion of capacity, become the most competitive link, and both the profit and industrial concentration will decline, leaving the five-year era of high profit.

Since 2016, monocrystalline silicon has gradually replaced polycrystalline silicon, and the technology generation gap has brought continuous excess profits. Longi (601012. SH), as the largest monocrystalline company, has naturally obtained the largest profits. Longi and TCL Zhonghuan have rapidly formed a duopoly monopoly pattern through massive expansion of production. Traditional component manufacturers such as Jinko Solar and JA Solar (002459. SZ) are unwilling to be constrained by others and also expand the production of silicon chips; At the same time, they have also cultivated third-party silicon chip manufacturers such as Shangji Automation and Beijing Yuntong, and the production capacity of single crystal silicon chips tends to be saturated.

Stimulated by the dual-carbon target, the silicon chip link with high profit and low threshold is more favored by capital. The excess profit is gradually eliminated with the expansion of production capacity, and the increase of silicon material price is accelerating the losing of silicon wafer profits. In the second half of 2022, with the release of the new capacity of silicon materials there is likely to be a price war at the silicon chip end. At that time, profits will be greatly squeezed, and some of the second-tier and third-tier production capacity may exit the market. The head enterprises should not rest assured. They should use their own advantages in scale, cost, technology and brand to maintain as much market share as possible. At the end of 2021, Longi and TCL Zhonghuan (002129. SZ) had become increasingly competitive, and the two sides had reduced their prices twice. Under the trend of silicon chip price reduction, the pressure bearing capacity of Longi and TCL Zhonghuan may be differentiated due to the degree of integration. By the end of 2020, the capacity of Longi silicon chip, battery and module is 85GW, 30GW and 50GW respectively; The TCL Zhonghuan is mainly composed of silicon chips and components, with the production capacities of 55GW and 4GW respectively. Longi's absolute advantages in silicon chip and component side enable it to flexibly adjust the proportion of silicon chip sold according to market conditions, so as to maximize profits. For example, when the market for silicon chips is poor, the proportion of silicon chips for self use can be increased and processed into component products for external sales; vice versa. In this way, TCL Zhonghuan with low degree of integration may be more injured in this round of price reduction, so the company is also rapidly increasing its component capacity. According to Caijing, by the end of 2021, the capacity of silicon chips and components in TCL Zhonghuan will reach 85GW and 11GW respectively.

All coins have two sides. Lv Jinbiao, deputy director of the expert committee of the Silicon Industry Branch, told Caijing that the component business was not entirely good for Longi, but also brought huge customer pressure. After establishing the absolute advantage of silicon chip, Longi entered the component business, directly competed with its customers for orders, and became the leader, which destroyed its industrial ecology. In contrast, TCL Zhonghuan has a more solid customer base and stronger viscosity, which is the advantage of TCL Zhonghuan in silicon chip price reduction. In addition to price, large size is also an important way for the two heads to compete for the market shares. Longi and TCL Zhonghuan have always been the main representatives of the 182mm and 210mm camps, respectively. However, TCL Zhonghuan recently launched products of 182mm and 218.2mm for the first time. This two sizes are the same, but it is said that 218.2mm has higher power, which is interpreted as an important signal for TCL Zhonghuan to seize Longi's 182mm market share. The "cross-border" behavior of TCL Zhonghuan indicates that there will be a battle in the silicon chip market in 2022. With the prices callback of upstream silicon materials and silicon chips, and the support of strong demand for downstream installation capacity, the profitability of battery chips and components will be repaired in 2022, and there is no need to be pinched.

PV manufacturing will form a new competitive pattern

According to the above inference, the most painful part of the photovoltaic industry chain in 2022 is the silicon chip sector with a serious surplus, among which specialized silicon chip manufacturers are the most painful. Conversely, the happiest one is still the silicon material enterprise, and the leading enterprise will make the largest profit.

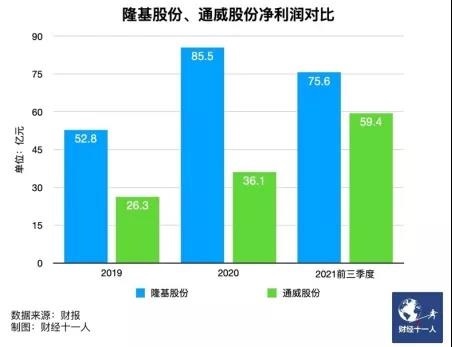

Longi became the leader of photovoltaic industry because of the excess profit of monocrystalline, Tongwei (600438. SH) is now catching up with the excess profit period of silicon materials, but the duration may not be long. In 2021, thanks to the high price of silicon materials, Tongwei will quickly narrow the net profit gap with Longi. In 2022, the price of silicon materials will still be high. Tongwei, as the leader, will make the largest profit, while Longi's silicon chip profit will further shrink. Tongwei is likely to surpass Longi and become the most profitable photovoltaic company. In 2020, GCL's global "No. 1" title in silicon materials and silicon chips has been replaced by Tongwei and Longi respectively. At present, in the four major links of photovoltaic manufacturing, Longi has reached the top at both ends of silicon chip and module, while Tongwei has reached the top at both ends of battery and silicon material. In terms of size and industry position, Tongwei has been comparable to Longi, so Tongwei is promising. "Although Longi 's market value is at a high level, the silicon chip has no absolute advantage, and the pressure to maintain and break through is increasing. Tongwei's silicon material advantage can still be maintained, and it is on the rise." A former senior executive of a photovoltaic enterprise believed that. Tongwei's production capacity has the advantage of late-development and has no historical burden, and there is a view in the industry that Tongwei is also slightly superior to Longi in terms of integrated layout mode . Both have common characteristics in strategic layout: they choose to strengthen one or two links first, and then expand up or down the industrial chain. However, in the initial process of integration, the two chose two different modes: self integration and seeking cooperation. On the premise of ensuring the absolute advantages of silicon materials and batteries, Tongwei guarantees its own demand for silicon chips through equity cooperation and complementation with Trina Solar (688599. SH), Jinko Solar, etc. The above executives believe that the current financing capacity of photovoltaic enterprises has been greatly enhanced, but the asset depreciation is also accelerating due to rapid technological progress. In this context, vertical integration is a double-edged sword, especially for the two sectors of battery and silicon material, which are invested too much. Collaboration is a good way. Due to the inconsistency of the involved industrial chain links, Longi and Tongwei have not yet had a "frontal confrontation", and the outside world does not often compare them together. However, the situation is expected to change soon. Tongwei has started to lay out its own production capacity in silicon chips and components this year, and will soon become the only enterprise with four manufacturing links in its head.

With the restructuring of industry profits and the influx of new players, the competition pattern of photovoltaic industry in 2022 will also be subject to great changes. "It's worth thinking about how to improve the size and resilience of the enterprise. Otherwise, when the market is mature and big enough in the future, you will not be the protagonist. " Wang Bohua, honorary chairman of China Photovoltaic Industry Association, issued a warning at the annual meeting in mid December. He believes that under the stimulation of the dual carbon target, more and more new entrants are investing in photovoltaic manufacturing, which brings great challenges to traditional photovoltaic enterprises and may cause fundamental changes in the industrial pattern. It is the first time in history that cross-border capital has entered the photovoltaic manufacturing end on such a large scale. New entrants always have the advantage of backwardness, and old players without core competitiveness are likely to be easily eliminated by new players who are rich and powerful. For example, the new player Gokin Solar announced at the end of last year that it would invest 17 billion yuan to build a 50GW silicon chip project. It only took 140 days from the formal signing to the trial production. The project speed has set the industry record, and the 50GW production capacity will be formed in 2022. According to the current planned production capacity, it is likely to become the third largest silicon chip manufacturer after Longi and TCL Zhonghuan by then.

Distributed power stations will no longer be supporting role

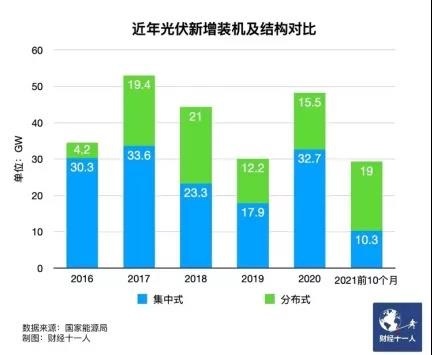

The power station is the downstream link of photovoltaic. In 2022, the installed structure of the power station will also show new features. Photovoltaic power stations can be roughly divided into centralized and distributed types, and the latter is subdivided into industrial, commercial and household use. Thanks to the policy of "promoting the whole county" and the policy of 3 cents per kilowatt hour electricity subsidy, household installed capacity has increased dramatically; However, the centralized installation has shrunk due to the price increase. In 2021, the distributed installation rate will probably hit a new record high, and the proportion of total installed capacity will also exceed that of centralized installation for the first time in history. From January to October 2021, the distributed installed capacity will be 19GW, accounting for about 65% of the total installed capacity in the same period, of which the household consumption will increase by 106% to 13.6GW, which is the main source of new installed capacity.

For a long time, the distributed photovoltaic market is mainly developed by private enterprises because of its dispersion and small size. In June 2021, the National Energy Administration issued the Notice on Submitting the County (City, District) Roof Distributed Photovoltaic Development Pilot Scheme, which clearly defined the integration of resources to achieve intensive development, and set off an investment boom in distributed photovoltaic throughout the country. A total of 676 counties were declared in 31 provinces. China Merchants Securities estimates that the potential installed space of distributed photovoltaic in China exceeds 500GW. This has aroused the strong interest of central enterprises such as State Power Investment Corporation, National Energy Group, Huaneng Group, and local state-owned enterprises, together with private enterprises such as Chint, Trina Solar, and Jinko. However, due to the inadequate understanding of policies and lack of overall planning by some local governments and enterprises, chaos frequently occurred in practice, and many counties and cities in China began to suspend or even suspend the filing of relevant projects and the approval of grid access. In the middle of December, Ren Yuzhi, Deputy Director of the New Energy Department of the National Energy Administration, pointed out that the next step would be to carry out distributed photovoltaic monitoring and evaluation, strengthen guidance, and promote in a standardized and orderly manner. In addition to the distributed market with broad prospects, the reserve scale of domestic photovoltaic power generation projects is also very strong. According to the statistics of China Photovoltaic Industry Association, at present, the scale of large base projects with a total of more than 60GW has been announced in China, and the configuration scale of photovoltaic power stations in 19 provinces (districts and cities) is about 89.28 GW. Based on this, the China Photovoltaic Industry Association predicts that the new installed capacity of PV will be more than 75GW in 2022, superimposed on the downward expectation of the industrial chain price.

Original link: https://qiye.qizhidao.com/article-hygc/1486310455608610817.html

Tel.:0512-68127800

E-mail:youngme@youngmeii.com

Address: F1-2, Building 12, No.38 Beiguandu Road, Yuexi Street, Wuzhong District, Suzhou City

©️ 2022 Jiangsu Younme IOT Intelligent System Co., Ltd. All rights reserved Powered by www.300.cn SEO